Compute in Plan A

Romeo Dean

This supplement explains our estimates and forecasts on compute-related numbers. It is divided into two major parts, the first pre-2029 and the second post-2029 (where it becomes conditional on Plan A). In the pre-2029 section, the main goal is to forecast the total amount of compute in the world year by year, and to break this compute down into informative categories, including AI-relevant and non-AI-relevant compute, single-devices vs. clusters, regional ownership, and datacenter sizes (for AI-relevant clusters). Post-2029 it justifies how much compute we think could be produced with AI acceleration of hardware R&D and production, as well as our forecasts for the concentration of compute in companies, the allocation of frontier AI compute between uses and our guesses about how AI copies-speed numbers will look in the Plan A scenario.

Summary in figures

| AI-relevant | non-AI-relevant | |

|---|---|---|

| Cluster | AI ClustersAI servers and pods. | Non-AI ClustersCPU servers. |

| Single-device | Specialty ConsumerHigh-end workstations and gaming cards. | Consumer ComputePhones, PCs, gaming GPUs. |

Two cutoffs define the split: a chip is AI-relevant if it clears the AI-compute performance floor, and a cluster if it is linked ≥ 5 GB/s to at least one other chip.

H100e added is annual capex × cost-efficiency (anchored to the 2024/25 actuals 5.09M, 13.6M, then forecast); installed stock is shown at the end of each year. The black bars are the EUV-constrained §1.1 buildout (~155M added in 2028, ~280M installed by end-2028); the red caps add China's off-EUV domestic manufacturing (§1.3), for a ~289M world total. Toggle ‘effective’ to rescale by the §1.2 usefulness factor.

Our forecast of all compute in the world, including AI-relevant and non-AI-relevant compute, measured in both raw H100e, and our effective H100e metric which makes an adjustment for memory and networking factors. World installed compute stock is measured at Jan 1st.

Owner = the nation of the company that owns or leases the compute. World compute is from §1.1; China is the §1.3.1 bottom-up forecast; the non-China remainder is split 85/15 US/RoW.

No deal vs Plan A, one year past the deal (through end-2029). Plan A collapses the debt-financed slice of capex (~31% off 2029 spending) while cash-flow-funded capex holds.

Plan A compute with different constraints lifted. The two constraints are the cap & trade policy in 2032, which restricts the quantity produced, and the hardware R&D deployment limits, which stop an exploding hardware R&D workforce from driving compute costs too low and chips too easy to manufacture.

Compute Definitions

Measuring compute: Raw vs effective H100e

The primary metric used in this supplement is H100-equivalents (H100e) multiples of one Nvidia H100 GPU measured in Total Processing Performance (TPP).

But compute isn't the only relevant hardware performance metric. The usefulness of compute for AI workloads also depends on many other factors, including memory bandwidth, memory capacity (stores and feeds data to the compute), and interconnect (to send data in between chips). Compute (H100e) is the headline metric we focus on but we also want to account for overall AI usefulness, so we also look at four other hardware resources, and combine them into an overall effective H100e metric:

| Resource | What it does | H100 (per H100e) |

|---|---|---|

| Compute (TPP) | the math throughput itself (defines the unit) | 15,800 TPP |

| Memory bandwidth | feeds data to the compute (HBM) | 3,350 GB/s |

| Memory capacity | stores data near the compute (HBM) | 80 GB |

| Scale-up | links chips within a server (NVLink) | 900 GB/s |

| Scale-out | links servers across the cluster (Ethernet) | 50 GB/s |

Effective H100e adjusts raw H100e (which counts compute alone) by a single usefulness factor .

is built from the four other resources in the table above. It adjusts for a chip's ability to actually be served by memory and communicate with other chips for representative AI workloads of its era, all relative to a 2024 100K H100 SXM cluster, which scores exactly .

Hardware that is memory-rich and well-networked for its FLOP/s can score above 1 (non-AI CPU servers, which carry lots of memory and networking around relatively little compute, score ~1.4), and e.g., compute with poor networking abilities (like gaming GPUs and phones) scores below one.

The usefulness factor is explained in full in the appendix.

Four categories of compute

The supplement attempts to model all the compute in the world and then partitions it in two independent ways giving four categories.

Partition 1: AI-relevant vs non-AI-relevant. A chip is considered AI-relevant if it clears all four floors of our AI-relevant cutoff thresholds set just below an A100 GPU.

| metric | cutoff | A100 | H100 | RTX 4090 |

|---|---|---|---|---|

| compute | 4,000 TPP | 4,992 | 15,800 | 5,285 |

| memory bandwidth | 1.0 TB/s | 2.0 | 3.35 | 1.01 |

| memory capacity | 32 GB | 80 | 80 | 24 |

| networking (NIC) | 100 Gb/s | 200 | 400 | 64 |

Partition 2: cluster vs single-device.

Cluster = is actively used in a multi-device setting with at least 2 devices connected at least at 5 GB/s bidirectional speed.

Single-device = actively used as a single device (e.g., a phone, a PC, a gaming card) or otherwise does not meet the cluster definition.

These definitions give us four categories of compute.

| AI-relevant | non-AI-relevant | |

|---|---|---|

| Cluster | AI ClustersAI servers and pods. | Non-AI ClustersCPU servers. |

| Single-device | Specialty ConsumerHigh-end workstations and gaming cards. | Consumer ComputePhones, PCs, gaming GPUs. |

Two cutoffs define the split: a chip is AI-relevant if it clears the AI-compute performance floor, and a cluster if it is linked ≥ 5 GB/s to at least one other chip.

Part 1. Pre-deal compute (pre-2029)

1.1 AI-relevant compute

In this section we forecast AI-relevant compute production with a demand-side method:

capex spent ($) cost-efficiency (H100e / $) = compute added (H100e)

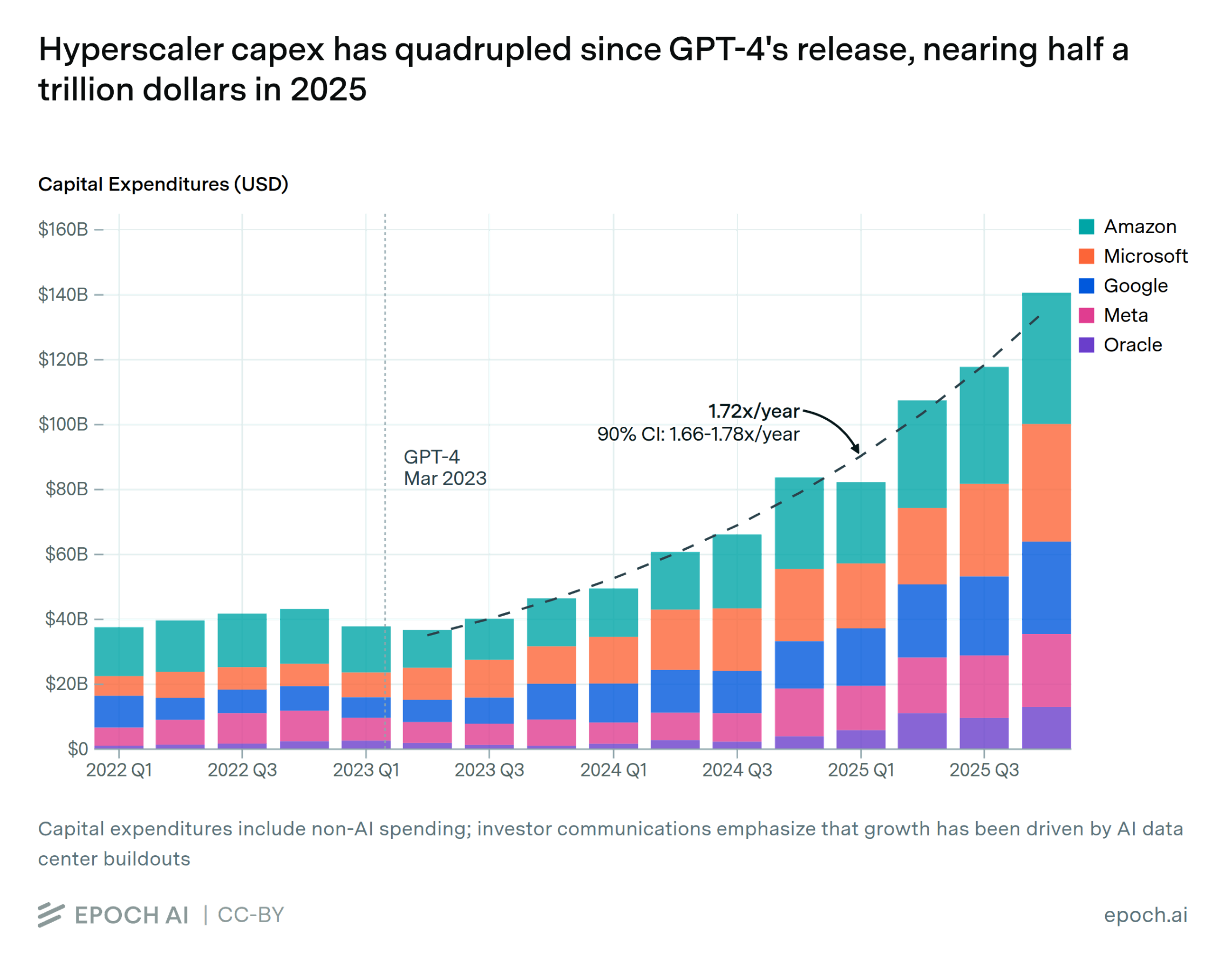

The AI capital expenditure trend has been ~1.72x/yr through Q3 2023 to Q4 2025, while cost-efficiency (H100e per dollar) has been improving around 1.4x/yr.

Source: Epoch AI — hyperscaler capex

Extrapolating these trends naively would lead to the following compute forecast:

The method is H100e added = capex × cost-efficiency, both extrapolated naively from the trends above (capex ~1.72×/yr; H100e per $ ~1.4×/yr). 2024/25 are actual Epoch data (AI Chip Sales: 5.09M H100e added on $260B spending in 2024, 13.6M from $448B in 2025).

The rest of this section will attempt to improve the forecast from this naive baseline.

Improving the capex forecast

Through 2025 the buildout was paid for almost entirely out of big-tech's operating cashflow. However, if this trend continues capital expenditures are on track to overtake operating cash flow of hyperscalers around Q3 2026.

To make a forecast that takes this into account, we split capex projections into three sources: existing-trend hyperscaler cash flow, AI cash flow (additional compute spend from AI company revenues, approximated as 80% of frontier AI company revenue forecasts), and debt & equity raises (which we are already starting to see grow in 2025/2026).

Our projections are as follows:

Existing-trend hyperscaler cash flow to continue growing at ~20%/yr (Epoch's ~$478B → $603B, with frontier AI company revenue stripped out) and deploy a rising share of it into the buildout, an invested fraction climbing ~75 → 85% as capex consumes more of cash flow.

AI cash flow to follow a total ARR (across frontier AI companies) of $30B (start-2026) → $180B → $500B → $1T (start-2029), with 80% of the recognized revenue counted as additional compute spend.

Debt & equity raises are hand forecasted (low effort) as a declining multiple of AI revenue: 3x (2025), 2.8x (2026), 1.8x (2027), 1.6x (2028). This is highly uncertain: on the one hand AI revenue growth motivates leverage, but as the total debt raise grows the interest rate will likely get higher. Note also that leverage at these levels implicitly conditions on the scenario's fast AI progress continuing (lenders keep believing in the revenue growth); like the revenue path itself, it is an input consistent with this scenario rather than an unconditional forecast.

With 2024-25 pinned to Epoch's Broad CapEx ($260B / $448B), this carries total AI capex to ~$2.4T in 2028, with debt reaching ~$900B (38% of the 2028 buildout). (We use hyperscaler Broad CapEx as the proxy for total AI capex: hyperscalers are ~60-90% of global AI spend, and ~60-90% of their capex is AI, and we assume the two gaps roughly cancel.) This is 7% higher than the naive baseline's (extrapolating the ~1.72x/yr trend) 2028 capex of $2.28T! This is because our bullish AI revenue forecast (and the debt raises we think its fast growth will motivate) actually pulls the trend slightly upwards.

Total AI capex = Epoch's hyperscaler Broad CapEx directly ($260B / $448B for 2024/25). We think hyperscalers are ~60–90% of global spend and ~60–90% of their capex is AI, so we assume the two roughly cancel as a simplifying assumption. Hyperscaler cash flow (existing trend) excludes frontier-AI revenue (to avoid double-counting) and we project it to grow ~20%/yr, with a rising fraction invested (~75→85%). AI cash flow is the additional compute spend from AI company revenues, approximated as 80% of frontier AI company revenue forecasts. Debt & equity raises we hand-pick as a declining multiple of AI revenue (3× / 2.8× / 1.8× / 1.6× for 2025–28), reaching ~$923B by 2028. This leads to ~$2.4T capex in 2028.

AI revenue and debt forecasts

Our AI revenue forecast follows a total frontier AI company ARR (annualized revenue run-rate) path of $30B → $180B → $500B → $1T (year-boundaries 2026.0 through 2029.0). Note that AI revenue is the flow recognized over the year, not the ARR run-rate, so this converts to annual recognized revenue of 2025: $15B / 2026: $84B / 2027: $313B / 2028: $721B. We count 80% of this as additional compute spend (the "AI cash flow" stream above) giving: $12 / $67 / $251 / $577B. Our total frontier AI company ARR projection is done manually and is highly uncertain. Broadly speaking we expect Anthropic's recent ~10x/yr ARR trend to slow down as they become the leading AI company in terms of revenue, and for the overall total AI company revenue trend to return to roughly 3x/yr, and slightly lower as companies manage to maintain roughly flat revenue / inference-compute ($/FLOP) while their inference-compute grows around 2x/yr in the later years. This is somewhat circular with the compute numbers, but is our current (highly uncertain) expectation.

What's a reasonable debt-raising rate given this revenue trend? For starters, the five hyperscalers issued ~$121B of bonds in 2025 (vs a ~$28B/yr 2020-24 norm), with BofA/JPMorgan projecting ~$175-300B in 2026; debt-funded neoclouds like CoreWeave carry ~4x revenue in debt ($21B on ~$5B revenue); and this Morgan Stanley podcast sees ~$1.15T of the ~$2.9T 2025-28 buildout as debt-financed. Total US investment-grade issuance is ~$1.5T/yr. The SpaceX IPO also shows the potential for large equity raises that might be followed with similar/larger ones by OpenAI and Anthropic. We use these anchors to manually set debt as an ad-hoc multiple of total AI revenue, 3x (2025) → 2.8x (2026) → 1.8x (2027) → 1.6x (2028), giving debt-financed AI capex of ~$36B / $188B / $452B / $923B over 2025-2028. That sums to ~$1.6T of debt-financed spending out of the ~$5.1T total buildout (2025-2028; ~31% debt-financed), roughly 39% above Morgan Stanley's ~$1.15T of debt, and ~75% above their ~$2.9T total, respectively, though notably Morgan Stanley's numbers ignore equity-raises.

Improving the cost efficiency forecast (supply-side)

The capex forecast is a demand-side forecast, while for cost-efficiency it makes sense to look at supply side. In particular, this section will focus on lithography (primarily EUV) capacity as the primary expected bottleneck on how many H100e can be produced.

EUV is needed for leading-edge logic, and the leading HBM DRAM nodes now use it too (DRAM was manufactured entirely without EUV until recently, e.g., Micron only adopted it in 2025, so this is a cost-optimality choice rather than a strict requirement; avoiding EUV just shifts the same demand onto the shared DUV pool). EUV is extremely hard to scale on short notice given the complexity of the machines and extensive supply chain dependencies, so we expect it to be the most important and informative bottleneck. Because of the time-inelasticity (how hard it is to quickly scale production in response to price signal), the EUV fleet is also relatively easy to forecast.

| Year | EUV fleet (start of year) | EUV added / yr | fleet passes / yr | AI logic wafers / yr | AI HBM wafers / yr | AI EUV passes / yr | AI share of fleet |

|---|---|---|---|---|---|---|---|

| 2024 | 220 | +44 | 87M | 0.2M | 1.1M | 7M | 7% |

| 2025 | 264 | +48 | 104M | 0.4M | 2.5M | 15M | 15% |

| 2026 | 312 | +65 | 124M | 0.7M | 4.6M | 34M | 27% |

| 2027 | 377 | +80 | 150M | 1.0M | 8.0M | 68M | 45% |

| 2028 | 457 | +100 | 183M | 1.6M | 13M | 118M | 65% |

| 2029 (no Plan A) | 557 | +125 | 223M | 2.1M | 17M | 172M | 77% |

EUV fleet over time and AI's usage share. The fleet starts at 220 operating tools in 2024 (we estimate ASML had ~127 EUV tools in use at end-2021, then shipped 54/42 in 2022/23, per ASML's annual reports; the full build-up with sources is in the details box below) and grows with its accelerating shipments. The EUV added column is ASML's shipments during the year (ASML guides "60+" for 2026 and ~80 for 2027). Fleet passes/yr is the during-year average fleet x ~360k passes/tool. AI's draw sums its logic wafers (x ~12-24 EUV layers per logic wafer, N4→N2) and its HBM-DRAM wafers (x ~4-7 EUV layers per HBM wafer, accounting for stacking and packaging yields). AI's share climbs ~15% (2025) to ~77% (2029, no Plan A).

How EUV scanners make a H100e

AI's claim on the fleet comes from both logic and memory, so we add the two in a single unit: an EUV pass = one EUV exposure of one wafer (a tool images ~360k/yr regardless of what it's printing). Here is the 2025 build-up.

1. Fleet → passes. Each scanner runs only ~40-50 wph-equivalent in practice, versus a ~160 wafers-per-hour nameplate: real patterns need longer exposures than the spec assumes (higher dose, limited by the light source's power), tools are only up ~75-82% of the time, and time is lost stepping between exposure fields (reticle overhead). Netting these out gives ~360,000 effective passes/tool/yr (the naive 160 wph x 8,760 h ≈ 1.1-1.4M is 3-4x too high). Two back-calculations agree: Frederick Chen (<50 wph effective) and SemiAnalysis (~1,500 wafers/mo x ~20 exposures). Starting from ~220 operating tools at the start of 2024 (ASML had ~127 EUV in use at end-2021, then shipped ~54 and ~42 in 2022-23; TSMC alone runs ~56% of capacity) the fleet does ~100M passes/yr in 2025, growing to ~220M by 2029 as ASML's EUV shipments accelerate (~48 in 2025 toward ~120/yr by 2029).

2. AI's logic draw. AI accelerators take ~0.4M leading-edge wafers in 2025, roughly ~12% of TSMC's ~3M ≤5nm wafers (Epoch's direct estimate; Blackwell on N4, Nvidia only now ramping into N3). At N4's ~14 EUV layers that is ~5M passes. (An ~800mm² die yields ~42 good dies/wafer at ~70% yield, per Cerebras; at ~28-36 H100e/wafer today → ~120 by 2029 as FP4 + the N4→N3→N2 shrink + Rubin's high H100e/chip compound, the all-logic ceiling is ~200M → ~1.2B H100e/yr. The shrink is not free EUV-wise: the model charges a growing pass count per logic wafer, ~12 in 2024 rising to ~24 by 2029, as more layers move onto EUV.)

3. AI's memory draw (the larger half). Essentially all HBM goes to AI, and HBM uses a lot of wafers per GB. Reported 2025 HBM TSV/back-end capacity is ~400k wafers/month (SK Hynix ~170k + Samsung ~165k + Micron ~60k, TrendForce), but that's a capacity ceiling, not utilized starts. Netting yields, AI's actual draw is ~2.5M HBM core-wafers/yr: a 24Gb-die DRAM wafer holds ~1,400 GB gross, and after ~57% core+stacking (KGSD/TSV) yield and ~88% CoWoS-assembly yield only ~700 net GB ship per started wafer, while the 2025 fleet needs ~1.8B GB of HBM (bottom-up: ~11.7M accelerators x ~150 GB, cross-checking the ~$35B / ~2B-GB industry total). The leading HBM nodes use real EUV (SK Hynix 1b ~4 layers, 1c ~6), so at ~4 layers that is ~10M passes, roughly two thirds of AI's EUV draw. (Per GB, HBM burns ~3x a DDR5 wafer.)

4. AI's fleet share. Logic (~5M) + HBM (~10M) = ~15M passes / ~104M fleet ≈ 15% in 2025. Rising HBM volume and EUV-layer count, plus AI's migration onto EUV-heavy N3/N2 logic, carry it to ~64% by 2028 and ~77% by 2029, with AI approaching saturation of the EUV fleet around 2029-30. This draw feeds back into the cost surcharge (more EUV use means a higher surcharge and fewer H100e per dollar), so it is solved self-consistently, and it is what trims the late buildout (2028 additions ~155M vs a naive ~190M).

5. Why passes and not wafer counts. AI's wafers are a mix: an HBM wafer takes only ~4 EUV passes while a leading-edge logic wafer takes ~14-22, so counting wafers treats very different claims on the fleet as equal. Since AI's wafer mix is HBM-heavy, a wafer count overstates its early share (it would put 2025 well above the ~15% the pass count gives). The two measures converge by 2029 for a simple reason: by then AI is the majority user of both the logic and the HBM wafer pools, so the mix difference stops mattering and either way of counting lands around ~80%.

AI's share of the EUV fleet grows from ~7% in 2024 toward ~64% by 2028 (and ~77% by 2029, near saturation). We expect this to translate to higher prices as it requires outbidding other uses of the fleet (e.g., phones, PCs, etc.). To model this, we implement a hand-chosen cost surcharge curve that depends on the fleet usage (highly uncertain ad-hoc choice).

Our forecast for % of global EUV time (passes) used by AI, including both logic and memory wafers (and accounting for yields). It runs ~7% in 2024 toward ~65% by 2028 (~77% by 2029), so AI hits the EUV wall around 2029-30. The cost surcharge (curve tab), surcharge = A·u^K (default A = 100%, K = 2.5), is keyed to this derived path and feeds back into the compute forecast (more draw → higher surcharge → fewer H100e), solved to a fixed point so it climbs to ~33% by 2028 and throttles the late buildout. The K and A sliders tune how hard it bites for users to play with. The parameters are hand chosen and extremely uncertain.

Applying this surcharge to the naive price-performance trend gives an updated compute cost-efficiency trend that averages ~1.25x/yr from 2025-2028 (and slows to just ~1.1x/yr by 2028 as the surcharge bites) instead of the historical ~1.4x/yr.

Cost per H100e decomposes as $ per wafer ÷ H100e per wafer.

Where the wafer numbers come from

The cost figure is an identity, $/H100e = (all-in $/wafer) / (H100e per wafer), and we have decent estimates of two of the three quantities, so we back out wafers per $B (the inverse of all-in $/wafer) as the residual and then check whether the wafer cost it implies is sensible.

$/H100e (known). 2024/25 are observed (annual capex / H100e added: ~$51K, ~$33K). For 2026-28 we take the ~1.4x/yr price-performance trend and penalize it by the EUV surcharge, giving ~$23K / ~$18K / ~$16K.

H100e per wafer (known, ~28 → ~98). An ~800mm² reticle-limit die yields ~64-72 gross dies per 300mm wafer, ~42 good at ~70% yield; netting downstream losses (packaging yield) leaves ~28 sellable H100e per wafer in 2024. This climbs ~1.4x/yr to ~98 by 2028 (~120 by 2029) from FP4/precision (EUV-free), the N4→N3→N2 shrink (paid in extra EUV layers), and Rubin's high H100e/chip, all reasonably well grounded in die-size, node, and precision estimates. (2025 check: ~13.6M H100e on ~0.38M AI leading-edge wafers ≈ ~36 H100e/wafer.)

Wafers per $B (the residual). Multiplying the two backs out the implied all-in $/wafer: ~$1.43M (2024) → ~$1.18M (2025) → ~$1.20M → ~$1.36M → ~$1.56M (2028), i.e. wafers/$B ~700 → ~845 → ~640. The 2025 dip comes directly from the observed data: 2024 was early and supply-constrained, and 2025 hit Blackwell volume, so all-in cost per leading-edge wafer fell. From 2026 the implied $/wafer rises, which is what we'd expect: TSMC ASP +5-10%/yr (N2 ~$30K, +10-20% over N3), CoWoS +15-20%/yr, datacenter $/MW rising, plus the EUV surcharge. The level also checks against a bottom-up build-up (foundry ~$25-30K + HBM ~$50-70K + CoWoS ~$10-15K, with a ~4-5x chip-designer markup giving a ~$400-500K accelerator, and the remaining ~$0.7-1.1M being the non-chip buildout: datacenters, power, land, networking). So the residual looks reasonable: wafer costs are a mild headwind after 2025, and the whole ~$51K to ~$16K decline in $/H100e comes from compute density improvements.

Multiplying this cost-efficiency baseline (incl. the scarcity surcharge) by the capex topline gives the annual H100e added (~155M in 2028), and an installed stock of ~280M by end-2028. We also adjust very slightly downwards for chip survival rates. China's domestically manufactured compute (§1.3) does not draw on this EUV supply chain, so we forecast it separately and add it onto this total, bringing the world AI stock to ~287M.

H100e added is annual capex × cost-efficiency (anchored to the 2024/25 actuals 5.09M, 13.6M, then forecast); installed stock is shown at the end of each year. The black bars are the EUV-constrained §1.1 buildout (~155M added in 2028, ~280M installed by end-2028); the red caps add China's off-EUV domestic manufacturing (§1.3), for a ~289M world total. Toggle ‘effective’ to rescale by the §1.2 usefulness factor.

Resource intensity: from raw H100e to effective compute

Even for the AI fleet, effective and raw H100e drift apart. The memory wall drags effectiveness below 1 (TPP, boosted by FP4, outgrows HBM bandwidth and capacity), while the growing coherent NVLink world (HGX-8 → NVL72 → NVL144 → NVL576) pushes it back up. The two roughly cancel: there is a mild premium in 2024 (~1.16, when the fleet is memory-rich) that fades toward ~1 by 2029 as the memory wall and larger training runs start to matter more. It is the same usefulness model as §1.2.3 (full derivation in the appendix); the deployment-weighted fleet inputs that drive it (scale-up world in H100e = coherent chips x H100e/chip):

| AI fleet (deployment-weighted) | 2024 | 2026 | 2028 |

|---|---|---|---|

| HBM bandwidth per H100e (GB/s) | 4,080 | 3,330 | 3,610 |

| HBM capacity per H100e (GB) | 110 | 91 | 85 |

| scale-up world (H100e) | 184 | 436 | 929 |

| H100e per chip | 1.15 | 2.58 | 5.34 |

| effective H100e per raw | 1.16 | 1.06 | 1.04 |

1.2 All compute

§1.1 forecast AI-relevant compute. Now we extend to all compute in the world. We split all compute into six device categories:

| Category | Examples | AI-relevant |

|---|---|---|

| AI | datacenter AI accelerators (H100, B200, MI300) | yes |

| Non-AI servers | datacenter CPUs and non-AI accelerators | no |

| PCs | laptops and desktops | no |

| Phones | smartphones | no |

| Gaming | gaming GPUs | no |

| Other | microcontrollers, automotive, edge | no |

Our method works by looking at two quantities. The device side is the compute we get from counting the units shipped and the average compute carried on each device. The lithography side is the compute the world can make, from counting the wafers the fabs can produce and the compute each wafer turns into.

device side H100e = units H100e per unit

lithography side H100e = wafers H100e per wafer

The compute per wafer is the quantity we are least sure of, so it is what we attempt to pin down from history (where we can get good estimates of all the other values).

1.2.1 Calibration (2015 to 2024)

Across 2015 to 2024 we look at device demand (units shipped and compute per unit) and lithography supply (wafers shipped), and use this to back out an estimate of compute per wafer that we can then use to forecast future compute by category based on wafer allocation and wafer supply forecasts (which are easier to do than device demand forecasts, because the supply side can be forecasted with the relatively predictable lithography ceiling).

Device side

| Shipments (M units/yr) | 2015 | 2018 | 2020 | 2022 | 2024 |

|---|---|---|---|---|---|

| phones | 1K | 1K | 1K | 1K | 1K |

| pcs | 276 | 259 | 304 | 292 | 263 |

| gaming | 44 | 50 | 40 | 38 | 36 |

| ai | 0.1 | 0.3 | 0.6 | 2.0 | 7.5 |

| non-AI servers | 8.0 | 11 | 13 | 14 | 13 |

| other | 12K | 20K | 24K | 28K | 30K |

Shipment sources

- phones: 1.43B (2015) → 1.24B (2024). Peak 1.47B (2016); pandemic trough 1.21B (2022). Source: IDC Worldwide Quarterly Mobile Phone Tracker / Omdia / Counterpoint.

- pcs: 276M (2015) → 263M (2024). COVID peak ~349M (2021), trough ~260M (2023). IDC runs ~30M above Gartner in 2020 to 2021 because IDC counts Chromebooks; we use the IDC basis. Source: Gartner / IDC PCD Tracker.

- gaming: discrete desktop add-in-board GPUs only (not iGPUs, not datacenter). 44M (2015) → ~35M (2024). Source: Jon Peddie Research AIB Report.

- ai: the whole AI datacenter; unit count = accelerators. TechInsights counted 3.76M NVIDIA datacenter GPUs in 2023 (98% share); 2024 is ~7.5M all-vendor (NVIDIA ~4M + Google TPU ~2.5M + AWS Trainium ~1.2M + AMD MI300 ~0.4M). Source: TechInsights via DCD; Epoch AI; Omdia/Morgan Stanley.

- other: just the advanced-node digital chips (networking ASICs, basebands, auto/IoT logic). The full MCU plus analog universe is far larger (~25 to 35B MCUs/yr alone), but most is trailing-node / 200mm capacity outside the 300mm lithography pool this model tracks.

| TPP per unit | 2015 | 2018 | 2020 | 2022 | 2024 |

|---|---|---|---|---|---|

| phones | 0.5 | 5.0 | 25 | 60 | 100 |

| pcs | 8.0 | 20 | 38 | 62 | 100 |

| gaming | 15 | 250 | 550 | 1K | 2K |

| ai | 350 | 1K | 2K | 5K | 10K |

| non-AI servers | 30 | 75 | 150 | 320 | 500 |

| other | 0.1 | 0.3 | 0.5 | 0.7 | 0.9 |

TPP-per-unit sources

TPP = (peak dense TOPS at a precision) × (bit-length of that precision), maximized over precisions: the US BIS export-control metric (ECCN 3A090). Anchors that fix the scale: V100 ≈ 2,000, A100 = 4,992, H100 ≈ 15,800, RTX 4090 = 5,285 (just over the 4,800 control line), B200 ≈ 36,000. All figures are sales-weighted averages, since the flagship is a tiny share of units. Sources: Federal Register 88 FR 73458, CSET explainer, Princeton ISCA 2025.

- phones: NPU INT8 TOPS × 8. Apple A11 = 0.6 TOPS (2017) → A17 Pro = 35 TOPS (2023); Snapdragon 8 Gen 3 = 45 TOPS (2024). Near-zero before 2017. Sales-weighted ≈ 100 TPP in 2024. Source: Apple Neural Engine TOPS table.

- pcs: most PCs have no NPU (only ~17% of 2024 units were “AI PCs”). Sales-weighted ≈ 100 TPP in 2024. Source: Canalys AI-PC share.

- gaming: dense INT8 TOPS × 8: RTX 3060 = 815, RTX 4060 = 1,412, RTX 4090 = 5,285. The sales mix is mostly xx60-class (Steam survey), so the sales-weighted average is ~1,500 TPP in 2024, not the 4090's 5,285. Source: Steam Hardware Survey.

- ai: sales-weighted across all vendors (H100/H200 = 15,800, A100 ≈ 5,000, TPU/Trainium lower), 2024 ≈ 9,500 TPP, below the NVIDIA flagship. With ~7.5M units that gives ~4.5M H100e in 2024, the bottom-up value that meets the Plan A forecast at the 2025 seam. Source: NVIDIA/Google/AWS datasheets; TrendForce mix.

- other: ~30B chips/yr, mostly MCUs/analog with ~0 AI throughput; only a thin automotive/ADAS + edge-NPU tail carries any, so the unit-weighted average is just ~1.5 TPP by 2024.

Lithography side

| wafers (M/yr) | 2015 | 2018 | 2020 | 2022 | 2024 |

|---|---|---|---|---|---|

| phones | 1.8 | 1.9 | 1.9 | 1.9 | 2.1 |

| pcs | 0.7 | 0.7 | 0.9 | 0.9 | 0.9 |

| gaming | 0.2 | 0.3 | 0.2 | 0.3 | 0.3 |

| ai | 0.0 | 0.0 | 0.0 | 0.0 | 0.3 |

| non-AI servers | 0.1 | 0.2 | 0.3 | 0.3 | 0.3 |

| other | 5.5 | 9.7 | 12 | 15 | 17 |

| device demand (total) | 8.3 | 13 | 15 | 18 | 20 |

Wafer shipment sources

- Each category's wafers = its logic wafers (units × dies-per-device ÷ good-dies-per-wafer) plus the memory wafers (HBM, DRAM, NAND) that ship with it. Units are the shipments table above. Memory wafers follow from each device's memory content and current per-wafer GB on DRAM/NAND/HBM nodes.

- Good dies per 300mm wafer (yield-net): phones ~600 (~100 to 120 mm²), PCs ~300 (~200 mm²), gaming ~130 (~400 mm²), AI ~42 (~800 mm² reticle-limit die at ~70% yield), “other” ~1,800 (~30 mm²). Sources: AnySilicon; reticle/die-size disclosures (TSMC, NVIDIA, WikiChip).

- Dies per finished device: non-AI ≈ 1 (one SoC/CPU/GPU per device). AI ramps 1 (H100) → ~1.5 (2024, dual-die B200) → ~8 to 11 by 2030 (Rubin-class chiplets). Sources: NVIDIA roadmap; SemiAnalysis.

- Die-area is already net of yield, so no separate yield factor is applied.

The lithography utilization by category is shown below. We treat every category as a package with its logic and associated memory (HBM, DRAM, NAND).

EUV exposure-passes drawn per year (the absolute view the share hides). Volume EUV begins ~2019; it's ~all phones/PCs early, AI invisible until ~2022.

Sanity check with independent compute per wafer estimates

Compute per wafer is just (good dies per wafer) x (TPP per die) / 15,800, both estimated from device specs independently of how full the fabs run:

Good dies per 300mm wafer (yield-net, from die areas; sources in the wafer box above): AI ~42 (an ~800 mm² reticle-limit die at ~70% yield), gaming ~130 (~400 mm²), PCs ~300 (~200 mm²), phones ~600 (~100 to 120 mm²), commodity 'other' ~1,800 (~30 mm²).

TPP per die = each category's TPP per unit (device side above) / its dies per device. In 2024 AI is ~9,500 / ~1.5 ≈ 6,300 TPP/die, gaming ~1,500, phones and PCs ~100, 'other' ~1.5.

So AI's big, high-TPP dies make it densest per wafer and commodity 'other' (tiny, near-zero-TPP dies) the lowest, which is exactly what dividing each category's compute by its wafers gives:

| implied H100e / wafer | 2015 | 2018 | 2020 | 2022 | 2024 |

|---|---|---|---|---|---|

| phones | 0.03 | 0.23 | 1.1 | 2.4 | 3.8 |

| pcs | 0.20 | 0.46 | 0.83 | 1.3 | 1.9 |

| gaming | 0.19 | 2.8 | 5.6 | 9.2 | 12.3 |

| ai | 1.4 | 5.0 | 7.2 | 14.2 | 16.8 |

| non-AI servers | 0.11 | 0.25 | 0.46 | 0.90 | 1.3 |

| other | 0.01 | 0.04 | 0.06 | 0.09 | 0.10 |

As a further check, the wafer demand these rates imply, set against our estimated lithography pool (broad global logic-wafer output, ~30M wafers in 2024, a scale consistent with SEMI's 300mm capacity), is ~62% to ~69% of the pool across the decade: a plausible, stable share that never runs past the pool. The pool level is itself calibrated to land in that range, so this says the die-size, compute, and capacity estimates are mutually consistent rather than independently validating any one of them.

The resulting H100e added each year by category is shown below in both raw and effective H100e:

Raw H100e added per year by category.

1.2.2 Forecast (2025 to 2028)

We take AI's compute forecast from §1.1 and ration the leftover lithography capacity to the other compute categories. AI first claims its lithography usage and then each non-AI category keeps its frozen-2024 share of the wafers that remain. That gives the projection:

| Flow (H100e/yr) | 2025 | 2026 | 2027 | 2028 |

|---|---|---|---|---|

| phones | 12.0M (33%) | 16.6M (25%) | 21.5M (18%) | 31.0M (14%) |

| pcs | 2.8M (7.7%) | 4.1M (6.2%) | 5.5M (4.5%) | 8.8M (4.0%) |

| gaming | 5.2M (14%) | 7.2M (11%) | 9.4M (7.8%) | 14.2M (6.5%) |

| ai | 14.2M (39%) | 35.7M (54%) | 80.6M (67%) | 159.7M (73%) |

| non-AI servers | 558K (1.5%) | 725K (1.1%) | 901K (0.7%) | 1.2M (0.5%) |

| other | 2.0M (5.4%) | 2.3M (3.4%) | 2.6M (2.2%) | 3.2M (1.5%) |

| total | 36.7M | 66.6M | 120.5M | 218.1M |

AI is from §1.1; non-AI gets the leftover logic wafers × rising TPP-per-wafer. Counting logic + HBM, AI reaches ~15% → 65% of EUV fleet capacity by 2028 (with the fleet ~100% utilized overall), but only ~40% of all logic wafers.

AI’s wafer claim, leftover pool, and bill of materials

| wafers/yr | 2025 | 2026 | 2027 | 2028 |

|---|---|---|---|---|

| AI logic wafers | 378K | 664K | 1.0M | 1.6M |

| + AI HBM wafers (advanced DRAM) | 2.5M | 4.6M | 8.0M | 12.8M |

| = AI cutting-edge wafers (logic + HBM) | 2.9M | 5.2M | 9.1M | 14.4M |

| % of EUV fleet capacity (logic + HBM) | 15% | 27% | 45% | 65% |

| % of broad lithography pool (all nodes) | 9.3% | 16% | 27% | 40% |

| allocatable logic pool (× util) | 20.9M | 22.0M | 23.2M | 24.4M |

| leftover for non-AI | 20.6M | 21.4M | 22.1M | 22.8M |

Sources: AI forecast and per-accelerator bill of materials

- AI H100e trajectory. From §1.1's EUV-constrained solve (capex topline ÷ cost-efficiency ÷ EUV surcharge): installed H100e stock (Jan-1) 8.6M · 22.4M · 57.1M · 135.2M → 289.0M by 2029, with annual production 14.2M · 35.7M · 80.6M · 159.7M. §1.2 takes this AI buildout from §1.1 unchanged and models only the non-AI leftover, so the two sections agree by construction. Source: §1.1 (resting on the Plan A capex topline).

- HBM per accelerator. H100 = 80 GB, H200 = 141, MI300X = 192, B200 = 192; sales-weighted ~130 GB in 2024 → ~600 by 2030. × ~7.5M units ≈ 1 EB HBM in 2024, matching the TrendForce industry figure. Source: NVIDIA/AMD datasheets; TrendForce.

- System DRAM & storage per accelerator. An 8-GPU node carries ~1 to 2 TB host DRAM (~150 to 250 GB/GPU) plus multi-TB local + networked NVMe. We model ~300 GB DRAM and ~2 TB NAND per accelerator in 2024 (growing to ~1 TB / ~6 TB by 2030), sized so HBM stays AI's heaviest wafer draw, not the commodity memory. Source: NVIDIA DGX/HGX H100 specs; hyperscaler reference designs.

- Stock vs production convention. AI's fleet is treated as cumulative (no retirement over this <5-yr window), so each Jan-1 stock is the running sum of production; we take the stock directly rather than running the bottom-up retirement recursion used for the non-AI categories. The production figure drives each year's wafer claim.

The rest of this section is the supply-side justification behind that table, i.e., what share of the lithography ceiling each category uses.

EUV exposure-passes drawn per year. AI's draw explodes, taking the fleet toward saturation by 2028.

Share of EUV and DUV passes that go to logic vs. memory

EUV utilization reaches ~100% by 2028 in our naive model, up from only 52% in 2024, as we expect it to become the binding constraint by then. That figure already separately accounts for uptime and realized throughput, both held at 2024 proportions. We don't expect utilization to literally hit 100%, but we're comfortable with the approximation: uptime and realized throughput (as a share of peak theoretical throughput) should improve a bit by 2028, roughly offsetting the gap.

| EUV pass pool (M/yr) | 2024 | 2028 |

|---|---|---|

| passes demanded | 45.3M | 182.5M |

| pass capacity | 87.1M | 182.5M |

| EUV utilization | 52% | 100% |

| immersion (DUV) utilization | 20% | 25% |

Utilization = passes demanded ÷ pass capacity. EUV and immersion are both on the effective (uptime- and throughput-adjusted) basis, so the two utilizations compare directly.

Node structure: passes per wafer and node mix

| node | EUV/wf | 193i/wf | wafers 2024 | wafers 2028 |

|---|---|---|---|---|

| logic tiers | ||||

| LEADING | 12→22 | 30 | 2.0M | 3.2M |

| DUVADV | 2 | 33 | 2.0M | 5.2M |

| MATURE | n/a | 6 | 16.4M | 16.0M |

| memory tiers | ||||

| DRAMadv | 4 | 12 | 4.2M | 20.7M |

| DRAMmat | n/a | 8 | 5.8M | 7.6M |

| NAND | n/a | 4 | 40.2M | 45.0M |

Three tiers (LEADING = ≤N3/N5/N2, EUV; DUVADV = N7/N16; MATURE = 28nm/legacy). Leading EUV passes/wafer climb 12→22 as the mix shifts N5→N3→N2. Red = EUV-drawing. This grid is a utilization diagnostic; it does not feed the compute or stock math.

Node mix (2024 wafer-area share by category)

| category | LEADING | DUVADV | MATURE |

|---|---|---|---|

| phones | 53% | 27% | 20% |

| pcs | 42% | 40% | 18% |

| gaming | 55% | 45% | n/a |

| ai | 95% | 5.0% | n/a |

| non-AI servers | 50% | 42% | 8.0% |

| other | n/a | 5.0% | 95% |

AI is ~all leading-edge; phones/PCs/gaming span leading to mature; “other” (MCUs) is ~all mature. The broad logic pool (29.5M wafers in 2024) feeds the non-AI allocation.

Per-device memory and wafer cost

Memory wafers = device count × per-device GB ÷ GB-per-wafer. HBM needs ~3× the wafer area per usable GB (8 to 12-hi stacks, TSVs, a base logic die) and goes almost entirely to AI, so an AI accelerator's memory outweighs its logic on wafers.

| per device (2024 → 2028) | HBM | DRAM | NAND |

|---|---|---|---|

| phones | n/a | 8 → 13 GB | 200 → 333 GB |

| pcs | n/a | 16 → 27 GB | 700 → 1033 GB |

| gaming | n/a | 14 → 21 GB | n/a |

| ai | 130 → 400 GB | 300 → 767 GB | 2000 → 4667 GB |

| non-AI servers | n/a | 512 → 683 GB | 26000 → 36667 GB |

| other | n/a | 0.05 → 0.05 GB | 2 → 3 GB |

- GB per wafer (2024): DRAM ~2,800, NAND ~21,000, HBM ~900; all grow ~1.7× by 2030. HBM is ~11% of DRAM wafers in 2024 (TrendForce: ~14%). Sources: SEMI; TechInsights; TrendForce.

- The non-AI server row carries the datacenter storage tier (SSD arrays, networked NVMe), so its NAND is large (~26 TB/server-equivalent); this folds in bulk storage a strict per-device count misses, landing world NAND ≈ 845 EB in 2024 (~44M wafers), in line with Trendfocus. Sources: TrendForce; Trendfocus; IDC / Omdia.

Litho supply sources: EUV layers/node, fleet, throughput, node mix

- EUV layers per node: N5/N4 ≈ 13 to 14, N3E ≈ 19, N3B ≈ 25 (double-patterned), N2 ≈ 23 to 25. A double-patterned layer needs two exposures, so passes ≥ layers; we model the leading tier climbing 12→24 (2024→2029). Sources: SemiAnalysis; WikiChip; TSMC.

- Memory EUV: advanced DRAM (1α/1β/1γ) uses ~1 to 6 EUV layers, ramping; 3D NAND uses none. We model advanced DRAM at ~4 EUV passes/wafer, mature DRAM and NAND at 0. Sources: SK Hynix / Samsung / Micron disclosures; TechInsights.

- EUV fleet: ~220 systems by 2024, ~457 by 2028 on ASML guidance. Throughput: ~360k effective exposures/tool-year (below the ~160 wph spec). Source: ASML.

- Immersion fleet: ~1,330 (2024) → ~1,800 (2028); abundant, so 193i never binds. Throughput: ~950k effective passes/tool-year (about half the ~1.8M nameplate run-rate, de-rated on the same uptime/throughput basis as EUV). Node mix is wafer-area share: Counterpoint ~43% of 2024 phone-SoC units on ≤5nm → ~53% of wafer area. Sources: ASML / SEMI; Counterpoint; TSMC.

1.2.3 Results

Accumulating production net of retirement gives the installed stock by category. Rescaling raw H100e to effective H100e (raw x , the resource-adjusted AI workload usefulness model derived in the appendix).

Effective H100e rescales each category's raw compute by a usefulness factor U, derived in the appendix.

| usefulness U | 2024 | 2026 | 2028 | 2029 |

|---|---|---|---|---|

| phones | 0.21 | 0.11 | 0.07 | 0.05 |

| pcs | 0.35 | 0.08 | 0.04 | 0.03 |

| gaming | 0.04 | 0.05 | 0.06 | 0.04 |

| ai | 1.16 | 1.06 | 1.04 | 1.02 |

| non-AI servers | 1.38 | 1.40 | 1.41 | 1.40 |

| other | 0.53 | 0.43 | 0.34 | 0.30 |

Per-chip inputs and the unclamped model output

The per-chip resource inputs that drive U, by category (2024). Only AI accelerators pair real compute with HBM-class bandwidth and a large NVLink coherent domain; every other category is effectively a single chip (scale-up world = 1). Non-AI servers are memory-rich but compute-light; consumer chips are bandwidth-poor and don't cluster; “other” (MCU / edge) is tiny on every axis.

| per chip (2024) | H100e/chip | mem BW (TB/s) | mem (GB) | scale-up world |

|---|---|---|---|---|

| phones | 4.0e-3 | 0.032 | 7 | 1 |

| pcs | 6.6e-3 | 0.085 | 12 | 1 |

| gaming | 0.097 | 0.41 | 11 | 1 |

| ai | 1.15 | 4.7 | 126 | 160 chips |

| non-AI servers | 0.030 | 0.70 | 512 | 1 |

| other | 5.7e-5 | 0.006 | 0.1 | 1 |

Over the forecast, H100e/chip roughly doubles every ~1.5 years while memory bandwidth and capacity per H100e fall (the memory wall) and AI's NVLink world grows (NVL72 → NVL576); the §1.1 resource-intensity box tracks the AI fleet's trajectory in full.

Raw U, before the non-AI ≤ 1 cap

| category (raw U) | 2024 | 2026 | 2028 | 2029 |

|---|---|---|---|---|

| phones | 0.21 | 0.11 | 0.07 | 0.05 |

| pcs | 0.35 | 0.08 | 0.04 | 0.03 |

| gaming | 0.04 | 0.05 | 0.06 | 0.04 |

| ai | 1.16 | 1.06 | 1.04 | 1.02 |

| non-AI servers | 1.38 | 1.40 | 1.41 | 1.40 |

| other | 0.53 | 0.43 | 0.34 | 0.30 |

Servers and “other” (MCU/edge) score > 1 because for a tiny-compute chip every per-FLOP ratio looks abundant, so the networking penalty all but vanishes and it floats to the compute ceiling. For non-AI servers this is plausible (genuinely memory-rich machines) and they are tiny in raw H100e (~1–2%), so we keep their raw U. For MCU/edge “other” it is an artifact, so we clamp it to ≤1; note “other” is a large raw share (~8–23%), so even the clamp at 1 likely overstates its AI usefulness.

Installed H100e by deployment quadrant; toggle raw↔effective and level↔share.

Cluster vs. single-device split. We also categorize compute into clusters and single-devices. Non-AI servers are treated as non-AI relevant clusters; phones, PCs, gaming GPUs and embedded chips are non-AI single-device; and AI relevant compute is almost entirely in accelerators run in datacenters (AI-relevant clusters), but there is a small rising amount of AI-relevant single-device chips that is negligible today and grows later as datacenter-class GPUs reach desktop form factors (e.g., NVIDIA's DGX Station).

| effective H100e stock (Jan 1) | 2020 | 2024 | 2026 | 2028 | 2029 |

|---|---|---|---|---|---|

| AI-relevant · cluster (AI datacenters) | 101K (4.1%) | 3.6M (26%) | 23.7M (67%) | 140.8M (90%) | 295.2M (94%) |

| AI-relevant · single-device (specialty consumer) | 0 | 0 | 0 | 218K (0.1%) | 938K (0.3%) |

| non-AI · cluster (non-AI servers) | 294K (12%) | 1.4M (10%) | 2.6M (7.5%) | 4.7M (3.0%) | 6.1M (1.9%) |

| non-AI · single-device (consumer) | 2.1M (84%) | 8.7M (63%) | 9.1M (26%) | 11.5M (7.3%) | 12.6M (4.0%) |

How we forecast AI-relevant single-device compute (specialty consumer)

These are standalone AI workstations: a capable GPU (≥1 TB/s bandwidth, ≥32 GB, ≥4,000 TPP) paired with a 100 Gb/s NIC, which clears all four AI-relevant floors. They range from workstations on RTX PRO 6000-class GPUs up to NVIDIA's DGX Station (one GB300, ~2.5 H100e). Cheaper minis like DGX Spark (~0.5 H100e) miss the bandwidth floor, and ordinary gaming PCs lack the 100 Gb/s NIC. At ~$10,000 to ~$100,000 each, they sell in modest volumes. We estimate units sold per year and H100e per unit, then add them up.

| shipping year | units shipped | H100e / unit | H100e added | installed (Jan 1) |

|---|---|---|---|---|

| 2026 | 15K | 2.5 | 38K | 0 |

| 2027 | 60K | 3 | 180K | 38K |

| 2028 | 180K | 4 | 720K | 218K |

| 2029 | 450K | 5 | 2.3M | 938K |

The installed (Jan 1) column is the running stock at the start of each year — exactly the specialty-consumer row in the table above (~938K H100e by 2029.0, about 0.3% of the AI fleet, ~255K units). The category is new, so the unit numbers are rough estimates.

1.3 Regional ownership

This section forecasts world compute ownership by region, for the AI-relevant compute from §1.1. We split ownership three ways: US, China, and the Rest of the World. We think it is most informative to focus on a separate Chinese compute forecast, because China is cut off from the main global supply chain by export controls, making it the hardest region to pin down with a crude percent-of-spending estimate.

What follows is therefore an independent Chinese compute forecast, broken down by the different sources of compute reaching China. We then make a crude estimate of the US versus Rest-of-World split of the global total. China's domestic manufacturing is treated as separate from the world compute total forecast in §1.1, because it does not come from the same (EUV-based) supply chain, so the §1.1 totals add it back on.

1.3.1 Chinese compute forecast

We categorize China's AI compute into four sources: Three come from the global supply chain (already in the §1.1 world total): legal imports (export-compliant chips: e.g., H20s historically, H200 under the current licensing policy), smuggled chips, and loopholes (chip dies smuggled in before packaging, or offshore datacenters Chinese firms own or lease from abroad). The fourth is domestically manufactured chips (SMIC 7nm logic / CXMT HBM / Ascend). China's compute grows ~9x over 2026-2029, but its world share still falls toward ~9% because the global buildout outpaces it.

The 2024-2025 anchors, pinned to observed data:

| Channel | 2024 | 2025 | Basis |

|---|---|---|---|

| Domestic | 0.25M | 0.6M | Ascend on SMIC ≤7nm + Cambricon, drawing a one-time foreign-HBM stockpile (~13M stacks, mostly Samsung ~11.4M ≈ 1.6M 910C) and a ~2.9M-die TSMC "die bank" (SemiAnalysis); ~0.8 raw H100e/910C |

| Legal | 0.2M | 0.15M | ~1M throttled H20s in 2024 (~0.2 H100e each); 2025 nets only ~0.15M: Q1 shipments before the April ban, a partial re-licensing from July, and Beijing discouraging purchases |

| Loopholes | 0.25M | 0.45M | offshore DCs Chinese firms own or rent abroad; the cumulative 2024+2025 total here (~0.7M by end-2025) sits just above the ≥~670K confirmed-rental floor (ByteDance ~520K) |

| Smuggled | 0.16M | 0.48M | grey-market banned parts, anchored to Epoch |

Forecasting 2026-2028

The three global channels are projected as a share of §1.1 world production:

| Global channel | Rule (share of §1.1 world) | 2026 | 2027 | 2028 |

|---|---|---|---|---|

| Smuggled | ~3.5% → 2% with more enforcement | 1.26M | 2.12M | 2.99M |

| Loopholes | ~2% (~1.5% confirmed-rental floor + other sources) | 0.7M | 1.6M | 3.15M |

| Legal | ~1% | 0.35M | 0.8M | 1.6M |

The legal channel could plausibly run 2-3x higher than this ~1% rule: the current licensing policy already covers volumes above it, though Beijing-side import restrictions push realized shipments back down.

Domestic is HBM-bound; see the recent SemiAnalysis CXMT piece:

| Domestic build-up | 2026 | 2027 | 2028 |

|---|---|---|---|

| CXMT HBM capacity (kwspm starts) | 30 | 55 | 100 |

| 8-hi stack yield (maturing) | 25% | 31% | 37% |

| good 8-hi stacks per wafer (~88 gross x yield) | 22 | 27 | 33 |

| → good 910C-equiv/yr (kwspm x 12k x stacks / 8) | 1.0M | 2.2M | 4.9M |

| raw H100e per 910C-equiv (logic + HBM3E gains) | 0.80 | 0.82 | 0.85 |

| → raw H100e on CXMT memory | 0.8M | 1.8M | 4.2M |

| uplift: smuggled HBM + other firms | +30% | +25% | +20% |

| = Domestic | 1.1M | 2.3M | 5.0M |

This is optimistic: we take CXMT's HBM ramp at face value (the SemiAnalysis CXMT piece projects it to ~12% of global HBM wafer supply by 2028), though that ramp is back-loaded (the 2026 column could plausibly be near zero) and competes with higher-margin commodity DRAM for the same fab.

DUV capacity is abundant. Ascend logic and CXMT memory both print on China's ArF-immersion (DUV) fleet; these AI chip projections only use a small fraction of it:

| DUV immersion fleet | 2026 | 2028 | Basis |

|---|---|---|---|

| Fleet (tools) | ~290 | ~400 | ~200 base + ~90 ArFi bought in 2024 (mostly NXT:1980Fi-class, 275-330 wph; 70% of ASML's 129, $5-7B); imports since slowed by Dutch controls (AEI) |

| Realized capacity (passes/yr) | ~520M | ~720M | fleet x ~1.8M realized passes/tool/yr (~5-6k wafers/day in production vs the ~2.4M nameplate; cf. §1.1's ~360k EUV) |

| Ascend logic | ~5M (~1%) | ~17M (~2%) | ~8 → 28 kwspm SMIC ≤7nm starts x ~40-60 passes/wafer (SAQP quad-patterning) |

| CXMT HBM | ~4M (~1%) | ~12M (~2%) | ~30 → 100 kwspm CXMT HBM starts x ~10 passes/wafer |

The AI draw is ~2% of fleet capacity in 2026, ~4% by 2028; the binding constraint is HBM. This is also why we don't expect China to simply flood its DUV fleet with AI chips: more Ascend logic without matching HBM doesn't add usable AI compute, SMIC's ≤7nm starts are capped by multi-patterning yield and cost rather than scanner availability, and most of the fleet profitably serves the mature-node economy (autos, industrial, appliances) that China is also trying to dominate.

The four channels combined (M raw H100e):

| H100e (per year unless noted) | 2024 | 2025 | 2026 | 2027 | 2028 |

|---|---|---|---|---|---|

| Domestic | 0.25M | 0.6M | 1.1M | 2.3M | 5.0M |

| Legal western | 0.2M | 0.15M | 0.35M | 0.8M | 1.6M |

| Loopholes (offshore DCs / rental) | 0.25M | 0.45M | 0.7M | 1.6M | 3.15M |

| Smuggled | 0.16M | 0.48M | 1.26M | 2.12M | 2.99M |

| Total added /yr | 0.9M | 1.7M | 3.4M | 6.8M | 12.7M |

| → China stock (end of year) | 1.3M | 2.9M | 6.3M | 13.2M | 25.9M |

| → China % of world | 14.7% | 13.1% | 11.1% | 9.7% | 9.0% |

1.3.2 Results

Combining the world total (§1.1), the China forecast (§1.3.1), and an 85/15 US/RoW split of the remainder gives ownership by region: the US holds the great majority throughout, China ~15% → ~9%.

Owner = the nation of the company that owns or leases the compute. World compute is from §1.1; China is the §1.3.1 bottom-up forecast; the non-China remainder is split 85/15 US/RoW.

1.4 Datacenter sizes

In this section we forecast how the AI compute from §1.1 will be distributed across datacenter sizes, from gigawatt-scale training campuses down to the long tail of small regional sites. The method is relatively naive (and uncertain). We take the total AI compute forecast (from §1.1), and spread it across a total datacenter count, fit a curve of datacenter sizes with three concentration anchors, and then split the result across the US, China, and the Rest of the World ownerships (from §1.3).

Datacenter sizes model

Setup. We take the total AI compute C (§1.1) and a datacenter count N (~1,000 sites in 2025, growing at a default 30%/yr to reach ~2,850 sites by 2029). We then allocate the datacenter sizes based on a size distribution.

Anchors. We pin the shape of the size distribution with three concentration anchors, the share of all compute held by the largest 1, 10, and 100 clusters, , which we forecast to be roughly 4%, 20%, and 70% (hand-set, adjusted up from Epoch's datacenter dataset), held flat over time:

Fit. We then model log-size as a cubic in log-rank, with four coefficients :

Those four coefficients are pinned exactly by four equations, the three anchors plus the total (a cubic in log-rank has four degrees of freedom, matching the four constraints, so the curve is fully pinned with no free parameters left over):

The first is immediate, since gives ; the other three are solved numerically. This recovers every datacenter size from just N, C, and the three anchors.

Regions. To split the curve across the US, China, and the Rest of the World, we forecast each region's ownership share of total compute (giving it a target ) and assign each datacenter to a region in proportion to that share. An optional skew can tilt a region toward smaller or larger sites (to match a region whose biggest clusters are known to differ, e.g. China) while keeping its total fixed, but it is off by default (), so each region is just a same-shape slice of the global curve.

Default parameters.

| parameter | default | what it controls |

|---|---|---|

| (sites in 2025) | 1,000 | datacenter count in 2025 |

| growth | 30% / yr | datacenter-count growth (→ ~2,850 sites by 2029) |

| 4% | compute share of the single largest cluster | |

| 20% | compute share of the largest 10 | |

| 70% | compute share of the largest 100 | |

| skew | 0 (off) | optional regional size tilt; 0 = proportional |

These concentration shares are hand-picked and uncertain, adjusted up from Epoch's observed current dataset on the assumption that it does not have full coverage of frontier clusters (its largest tracked sites cover ~15% of global AI compute as of late 2025).

Part 2. Post-deal compute (post-2029)

In this section we forecast what happens after Plan A is implemented, as well as the 1-year default counterfactual without Plan A.

2.1 The no-deal counterfactual

To predict one more year of the default (no-deal) path, we extend the §1.1 method (and §1.3 for China's domestic additions) to the installed stock at the end of 2029. Under Plan A we expect the temporary R&D pause and general uncertainty during the deal's implementation to make capital spending temporarily lower. We approximate this by having the debt-financed slice of the buildout collapse to zero under Plan A, while cash capex stays on trend. With the fast implementation of inference-only verification and increased inference-compute allocation, we expect the AI revenue forecast to stay on par with the default counterfactual.

Overall, we think a good implementation of the deal can provide confidence to companies that R&D will be allowed to resume, and that given the level of realized capabilities and continued improvements once R&D resumes (which will be at a slowed down but still fast pace), we expect AI investment to still be extremely economically attractive. We expect this to hold despite increased transparency, because without algorithmic moats the economic value will accrue to the owners of compute (who can therefore still be the ones to train the best models first and serve them to the widest user base).

No deal vs Plan A, one year past the deal (through end-2029). Plan A collapses the debt-financed slice of capex (~31% off 2029 spending) while cash-flow-funded capex holds.

2.2 AI-relevant compute after the deal

Further into Plan A, we have increased uncertainty over compute growth, especially as AI and robots become capable of automating hardware R&D and production, and drastically increasing the previously human-constrained workforce. Given the uncertainty, we think it is reasonable to use a relatively simple model (Jones and Wright's-law learning) that takes the §1.1 compute path as its starting point and runs it to 2040. Given the hardware explosion we expect by default with unconstrained AI and robot deployment on hardware R&D and production, and the fact that this would be destabilizing (among other things, increasing the ease of defecting on the deal and verification burden within the deal) Plan A features a cap-and-trade regime to slow down the hardware explosion to controllable (but still drastically increased) hardware levels.

Why we expect hardware to grow fast. We can think of two separate forces lowering the cost per unit of compute:

Design improvements (modelled with Jones). Design improvements can lead to more compute per fixed unit of AI chip production, with better chip layouts, memory designs, transistor density, packaging etc. This is R&D, so we can model it with the labor spent on it, but with diminishing returns as the easy ideas get used up (Jones 1995, calibrated by Bloom et al. 2020) and with diminishing returns to more parallel labor at a given time. Think of this as the historical improvements in 'compute per wafer' (including node shrinks, which we bucket under design R&D since they come from chip and equipment research rather than from production scale). Roughly 2 million people work in semiconductors today; by the early 2030s our forecast is that combined human, AI, and robot effort on chip and equipment R&D is on the order of 100x that. Under our model's parameters this only speeds up the 'Moore's law' progress by around 1.1x.

Production scaling (Wright). Pure manufacturing scale of units of compute can lead to 'learning by doing' efficiency improvements, e.g., with yield, throughput, uptime effects, and economies of scale. Think of this as the improvements in 'wafers per dollar' historically. We model unit cost falling about 15% per doubling of cumulative production (similar to long-run semiconductor and solar rate). We don't know if AI and robots automating fab construction and operation will speed up this trend, but at least think it's a reasonable baseline that these gains from scale will continue separately to design improvements.

We treat the cost per unit of compute ($ / H100e) as the product of the two factors (compute / unit produced) and (units produced / $), where historically the unit has been 'wafers' but may change with future paradigms. Each factor is normalized to 1 in 2025 and falling thereafter. We take the §1.1 endpoint as the starting point and run these two models forwards to 2040.

The Jones & Wright's-law cost model

The cost per unit of AI compute is one 2025 anchor times two indices that both start at 1 and fall over time, a manufacturing index and a design index :

Wright's law (manufacturing). Cost falls with cumulative production, the classic learning curve:

so each doubling of cumulative output cuts manufacturing cost by . We use , about 16% per doubling, similar to the long-run semiconductor learning rate (close to Swanson's law for solar).

Jones design R&D. The annual design-cost decline scales with more labor doing R&D, with diminishing returns:

where is combined human and AI cognitive labor (which scales with deployed compute) which is taken from the 'effective labor' quantity from our economic model that combines AI / robot labor quantities with its capability (% of tasks it is able to automate). is the base pace, and is the "stepping on toes" adjustment (Bloom et al. 2020): a 100x research force buys far less than 100x the progress.

| Parameter | AI chips |

|---|---|

| Wright learning | 0.25 (~16% / doubling) |

| Jones base rate | 25% / yr |

| Jones stepping-on-toes | 0.05 |

| 2025 cost to make | $5,000 / H100e |

| Cumulative output, 2025 | 20M H100e |

The base rate (25%/yr) tracks the ~1.35x/yr compute-efficiency trend, and keeps stepping-on-toes strong: a 100x AI research force buys only ~1.3x the design-progress rate, so even the swelling AI workforce only modestly accelerates chip design. The anchor above is the cost to make a chip (marginal production cost, ~$5K in 2025), which is what the cost figure tracks; markups plus datacenter and power bring the all-in cost to ~$33K, which is what the $-invested figure counts. Both fall along the same curve. Below we run this loop with and without Plan A's two constraints, the compute cap and the R&D controls.

The hardware explosion has two throttles in Plan A. Without them there is too much progress for the deal's stability (ease of defection and verification burden). There is a feedback loop where more compute leads to more hardware R&D and production, leading to more compute and cheaper hardware. Plan A has two constraints that act on different parts of that loop: capping production levels (cap-and-trade policy from 2032 onwards) and limiting R&D deployment (to avoid compute becoming too easy and cheap to manufacture despite the quantity caps).

Plan A compute with different constraints lifted. The two constraints are the cap & trade policy in 2032, which restricts the quantity produced, and the hardware R&D deployment limits, which stop an exploding hardware R&D workforce from driving compute costs too low and chips too easy to manufacture.

Assumptions for each scenario

All three scenarios follow Plan A's compute path until the cap starts to bind (~2034), then differ on two levers:

Compute cap (cap-and-trade, 2032 on). On: installed compute is pinned to the Plan A policy path, ~1T H100e by 2040. Off: an unconstrained reinvestment loop sets the quantity and it runs away.

Hardware R&D. Controlled: chip-design progress is held to its historical Moore's-law pace. Unconstrained: the hardware-R&D effective labor is the economic model's effective AI labor (capability x quantity), so the design-cost decline accelerates with it (base rate 25%/yr, stepping-on-toes , capped at 60%/yr).

| Scenario | Compute cap | Hardware R&D | What happens |

|---|---|---|---|

| Plan A | on, ~1T by 2040 | controlled | the bounded path the rest of the document uses |

| no cap, hardware R&D controlled | off | controlled | quantity explodes to thousands of times the cap |

| no cap + hardware R&D unconstrained | off | unconstrained | quantity and cost both run away, off the chart |

Effective labor is the same series in every scenario (the econ model's A_eff, capability x quantity, scaled by that scenario's compute); the R&D control acts on how much of it becomes design progress, not on the labor total:

| Hardware R&D | effective AI labor, 2040 (HE = human-equivalents) | design-cost decline |

|---|---|---|

| controlled (Plan A) | ~400B HE | ~10%/yr, held at the historical Moore's-law pace |

| controlled (no cap) | ~2x10^15 HE | ~10%/yr, still held despite the vastly larger workforce |

| unconstrained (both) | ~2x10^21 HE | 25%/yr, scaling to a 60%/yr cap |

The unconstrained rate is exactly the economic model's Jones formula (25%/yr x (A_eff growth)^0.05, ); the controlled cap is Plan A's R&D-control policy layered on top, which the base economic model does not impose.

What share of effective labor does R&D? A fixed, constant share of the effective labor; only its growth matters, so the share cancels and we do not commit to a specific percentage. That effective labor is the economic model's effective AI labor (A_eff, capability x quantity), scaled by each scenario's compute relative to Plan A, so R&D progress responds to both rising capability and rising quantity. Robots are held on their fixed Plan A cap-and-trade path and are not varied across these scenarios.

Supply-side implications and sanity check.

The compute production possible by default in Plan A is modelled relatively naively, and the cap-and-trade trajectory is set considerably lower due to other constraints (verification and deal stability). In this box we motivate the cap-and-trade trajectory being possible with an illustration of what it implies on the supply side. In particular we look at the lithography it would require compared to historical growth.

Method. We take Plan A's annual production (new H100e per year, rising to roughly 570 billion H100e/yr by 2040) and convert it to silicon wafers (assuming this remains the paradigm), convert the wafers to lithography exposure-passes needed and then divide by one lithography machine's throughput (realized passes per machine-year) to get the machine-years needed.

Default lithography fleet. We anchor at 2029 (about 0.7 EUV passes per H100e, from §1.1) and compare against the lithography fleet on its historical path (about 620 operating machines in 2029, growing roughly 20%/yr; ASML ships about 125/yr today). We also let machine throughput rise about 10%/yr, matching the historical climb in wafers-per-hour (roughly 125 to 220 over 2019 to 2024).

Default compute density. Over time H100e/wafer has been increasing around 35%/year; we look at three different possibilities for the lithography buildout it would imply vs. the default trend.

| compute-per-wafer growth | 0%/yr (frozen 2029 tech) | 35%/yr (continued tech trend) | 50%/yr (faster tech trend) |

|---|---|---|---|

| lithography machines needed by 2040 | ~1,100,000 | ~14,000 | ~4,400 |

| vs the fleet's historical trend (~4,300 by 2040) | ~255x | ~3x | ~1x |

| implied annual production vs today (~125/yr) | ~4,400x | ~29x | ~6x |

We expect something like the middle column to be what happens in Plan A.

We can also express Plan A's buildout in dollars, as a check on the investment it implies. Each year's implied investment is the compute added that year times an all-in cost per H100e, which is the production cost from the model above times a markup covering everything else a dollar of AI capex buys (chip-maker margin, datacenters, power, networking). We calibrate the markup so that 2025 to 2028 reproduce Part 1's capex forecast exactly (~$2.4T in 2028) and 2029 the §2.1 deal year: this gives roughly 7x to 8x. Our best guess is that the markup then declines to ~1.2x by 2040, since robot-built fabs and datacenters should sell hardware near production cost, and the power and datacenter share of each H100e shrinks with the efficiency gains below.

We are very uncertain about the uncapped paths, but we think the unconstrained default is likely to be orders of magnitude higher than our capped path. The effective labor available for hardware R&D and chip production scales enormously once AI and robots are capable of that work. We think the stacked Jones and Wright's-law learning-curve dynamics are a reasonable naive approximation of what this might look like.

Historically, chip design improvements have been closely tied to power-efficiency improvements, so we model compute power efficiency on the same Jones design trend as the cost model above, using the same parameters (25%/yr base rate, stepping-on-toes ) at Plan A's constrained R&D pace, which leads to the following trajectory (notably not breaking past the CMOS transistor theoretical limit that Epoch estimates).

Total facility power per H100e (in Epoch's terms: chip TDP plus the server's other components plus cluster-level overhead like cooling, i.e. the full power draw at the grid), fleet stock-average, from the econ model's Plan A energy trajectory (same constrained Jones design trend as the cost model). It reaches ~37× the 2025 chip by 2040, still several× above the CMOS practical limit Epoch estimates (~200× a current H100e).

2.3 Company concentration

In this section we show our projections for how compute is distributed among companies over time. We track AI company end-users (the company that actually uses the compute) as opposed to owners (who may use or rent their compute to others). Early on most compute is owned by hyperscalers in a concentrated way (Google owns ~25% of compute) but the AI company end-users are less concentrated, with the largest using around 10% of global compute in 2026 (GDM and OpenAI are similar).

The share used by AI companies has been growing over time, and we project this trend forwards until Plan A is implemented. After 2030 the Plan A transparency regime lowers barriers to entry: investment in AI grows and spreads more evenly, and compute becomes distributed across more companies. By 2040 the largest holds only about 5% of world compute and there are around 20 frontier companies (defined as anyone within 4x of the largest).

Method for company compute concentrations

The method is relatively naive, where we set one worldwide rank-size law for the shape of the distribution, hand set to match forecasts, and then companies are assigned to ownership regions to match the §1.3 split. Across a universe of end-users worldwide, the share of the rank- company is

normalized so the shares sum to one ( is the standard-normal quantile of rank ). It has two shape parameters: sets the overall spread (concentration, which drives the top three), and is a head tilt that decays as , moving the single leader relative to the next two with less effect on the tail.

We choose the world's top-1 and top-3 end-user shares directly each year and solve so the distribution reproduces both. The leader is a minority early (frontier AI companies don't yet use most AI compute), rises into the 2029 deal to about a fifth of world compute with the top three at nearly half, then both decline as Plan A spreads compute (top-1 about 10% by 2035 and 5% by 2040; top-3 about 25% then 13%). A better justification of this forecast is currently future work. We wanted to create a model of "AI market power" / "willingness to pay" for AI compute that was a combination of algorithmic IP (which becomes uniformly distributed after the deal), non-algorithmic IP/capital (datasets, users, brand loyalty, talent loyalty, etc.) and finally capital more broadly, and build a model of compute allocation over time tracking this quantity. This was complicated though and we ran out of time.

Each company is then assigned to an ownership region (US, China, rest-of-world) by a hard-capped greedy fill, so regional totals match the §1.3 ownership split exactly every year through 2029 and then matching the Plan A ownership splits which converge towards the cap-and-trade deal allocations. A per-region size bias shifts only which companies a region holds, never its total: the US is neutral and holds the biggest developers; China is flat and dispersed through 2030, then a state-backed core consolidates at 2031 (its top developer jumps to about half of China's compute and lands a frontier developer) before gradually flattening again by 2040; the rest-of-world is flatter and flattens further toward the end, so the single largest developer worldwide stays in the US even once the rest-of-world's ownership share overtakes it.

Through 2030 (the deal era) the frontier set is the three largest end-users worldwide (the leading US developers are named, in a hand-set per-year order). From 2031 we drop names and call an end-user frontier if it is within 4x of the largest end-user worldwide.

| parameter | value | role |

|---|---|---|

| worldwide end-user universe () | 200 | the rank-size law's company count |

| top-1 end-user share (2026 / 2029 / 2035 / 2040) | 8% / 20% / 10% / 5% | hand-set; solved to match |

| top-3 end-user share (2026 / 2029 / 2035 / 2040) | 23% / 45% / 25% / 13% | hand-set independently of top-1 |

| §1.3 ownership split at 2040 (US / CH / RoW) | 35% / 20% / 45% | regional totals matched exactly each year |

| China size bias | flat, then +5 at 2031, easing to +2 by 2039 | dispersed early; consolidates at 2031; flattens by 2040 |

| rest-of-world size bias | −0.6, to −2.5 by 2039 | flattens toward the end so the US keeps the largest developer |

| frontier rule | top-3 (≤2030) / within 4x (≥2031) | deal era names the top three; later, within 4x of the largest |

2.4 Compute allocation

In this section we forecast allocation of frontier AI compute in Plan A. In 2025 OpenAI spent around half of its compute on inference and more like one third on inference in 2024 and the rest on training and experiments (of which only around 10% on final frontier training runs). We project this current split forwards naively until the 2029 deal, and then forecast each share conditional on Plan A.

2.5 AI copies and speed

In this section we forecast how many copies of the frontier model can be run at once and at what token/second speed. These are both imperfect metrics, because it may be difficult to know how to count a 'copy' under different scaffolds / architectures in the future, but we assume each parallel instance of the model weights being served, so copies = replicas x batch. Speed is also imperfect, because we probably care more about the speed of task completion, but we just focus on decode tokens per second, even though the speed comparison in tokens might break down with future paradigm changes, e.g., neuralese instead of chain of thought.

Up front: these forecasts are concrete best guesses, and we think the honest uncertainty is multiple orders of magnitude. Both the AI paradigm (architectures, sparsity, agent scaffolds, whether 'copies' is even the right frame) and the hardware paradigm (the memory and bandwidth tradeoffs of chips, how much silicon gets specialized for inference) could change several times before 2040. The method itself is simple, and we prefer to state it plainly: we guess the frontier model's size, we guess what share of the world's compute runs inference, and then we get copies by dividing the inference fleet's total memory by the bytes each copy takes, and we get speed from how quickly memory bandwidth can read the bytes each token needs. The rest of this section explains how we make each of these guesses.

Model size. We combine the global compute growth from the previous sections with the leading company's concentration (§2.3) and training allocation (§2.4) to get frontier training compute over time (roughly 32x today's by 2029 and 160,000x by 2040). We then map these compute numbers as well as a sparsity forecast to model size (total parameters) with a simple model:

Where is total parameters (T, today's level), is frontier training compute, and is sparsity. The compute exponent is the sensitivity of model-size scale up to compute scale up. Simple Chinchilla-optimality implies ~0.5, but we have wide uncertainty; there are reasons it might increase, e.g., due to data availability (fitting our formula to Nesov's own compute and sparsity numbers gives ), or for example, intentional undertraining due to e.g., making it harder to steal the weights. There are also reasons it might decrease, e.g., more overtraining for serving (Sardana and Frankle), reinforcement learning, and other unknown unknowns about paradigm changes. We just assume and draw as a range on the figure to show what we think is a plausible range. The sparsity exponent is tentatively better pinned (though the sparsity MoE paradigm might change).

We think it's valuable to include the sparsity assumption because it might affect the speed and copies significantly.

total = 10T × (compute growth)α × (sparsity growth)β, with α = 0.5 and β = 0.74.

| Year | 10T × computeα | × sparsityβ | = ours (total) | α ∈ [0.2, 0.8] | Nesov |

|---|---|---|---|---|---|

| 2026 | 10T | x1.0 (8x) | 10T | 10T to 10T | 10T |

| 2027 | 20T | x1.7 (16x) | 33T | 22T to 49T | 30T |

| 2028 | 35T | x2.8 (32x) | 97T | 46T to 205T | 240T |

| 2029 | 57T | x2.8 (32x) | 158T | 56T to 449T | 650T |

| 2030 | 83T | x3.1 (37x) | 255T | 72T to 904T | — |

| 2032 | 229T | x3.8 (48x) | 862T | 132T to 5,638T | — |

| 2035 | 1,411T | x4.7 (64x) | 6,576T | 337T to 128,155T | — |

| 2040 | 3,992T | x7.8 (128x) | 31,063T | 854T to 1,129,715T | — |

Differences with Nesov's numbers

How Nesov gets 650T: Both Nesov's forecast and ours start from training compute; the difference is mainly that Nesov's 2029 frontier run is 2x larger at 8e28 FLOP assuming 30x sparsity. At 30x sparsity compute-optimal ratio is 240 tokens per active parameter (from a sparse-MoE scaling paper) so 8e28 FLOP would want 7.4T active parameters on ~1,800T tokens. But he assumes only ~200T tokens of unique data exist, an 8.5x shortfall, which he splits with this data-constrained scaling result to get roughly 2.9x more active parameters (7.4T → 22T) and 2.9 epochs of repetition. We don't make the same low-data-regime adjustment as Nesov, because we think multiple factors such as more reinforcement learning, changes to the training paradigm, synthetic data generation, etc. could pull the other way. Given the uncertainty on these factors that could pull in both directions we prefer to use a naive simpler baseline.

From “Model size scaling in 2023–2031”.

| Year | Pretraining compute (FLOP) | Sparsity | Active params | Total params | Data shortfall | Epochs |

|---|---|---|---|---|---|---|

| 2026 | 1.3e27 | 8x | 1.3T | 10T | — | 1 |

| 2027 | 6e27 | 8x | 2.9T | 30T | 1.75x | 1.3 |

| 2028 | 2e28 | 30x | 7.9T | 240T | 4.5x | 2.1 |

| 2029 | 8e28 | 30x | 22T | 650T | 8.5x | 2.9 |

| 2030 | 1e29 | 30x | 26T | 790T | 10x | 3.1 |

| 2031 | 2.2e29 | 30x | 48T | 1,400T | 15x | 3.9 |

Inference-compute fleet. We take the §2.4 inference share of world compute (public + internal), and hold its memory and bandwidth per H100e ratios (§1.1) flat after 2029. We split this compute into ordinary general-purpose chips and inference-specialized chips, a hand-set scenario we describe below.

Serving memory by chip type (exabytes, log). Specialized memory is derived from demand (replica weights + KV per copy): ~2.3 ZB by 2040 vs ~10 ZB general-purpose.

Concurrent frontier copies served (replicas times batch), 2026 to 2040 (log).

Copies. We get copies by dividing the inference fleet's total memory by the bytes each copy takes. Each copy needs its share of the model weights (a full set of weights is ~5 TB today at 4-bit, and ~15 PB by 2040 at our central model size, shared across the copies served in the same batch) plus its own context. Rather than modelling batch sizes and KV caches in the main text, we just state their combined effect: we assume context takes up about half of general-purpose inference memory today, falling to ~5% by 2040 because the weights grow much faster than each copy's context does (the details are in the method box, and the batch assumption just trades off with context length assumptions and is arbitrary). This gives about 30 million copies today. The count dips slightly at first, because the jump in sparsity grows the model faster than the inference fleet, and ends up at very roughly 200 million by 2040, with most copies on general-purpose hardware and the rest being the much faster copies on inference-specialized chips described below.

| Year | Avg context | KV / copy | Context / replica | Weights / replica | Context share |

|---|---|---|---|---|---|

| 2026 | 200k | 20 GB | 5.1 TB | 5.0 TB | 51% |

| 2029 | 341k | 68 GB | 17.4 TB | 79.2 TB | 18% |

| 2032 | 580k | 220 GB | 56.3 TB | 430.9 TB | 12% |

| 2035 | 988k | 896 GB | 229.3 TB | 3.3 PB | 7% |

| 2040 | 2.4M | 3.3 TB | 856.1 TB | 15.5 PB | 5% |

Model size, copies, and speed at milestone years (Plan A).

| Year | Model (total/active) | Copies (gen/inf) | All copies | Speed (gen/inf) | Avg speed | Total tok/s (gen/inf) |

|---|---|---|---|---|---|---|

| 2026 | 10T / 1.3T | 30.3M / 8k | 30.3M | ~57 / ~1.0k | ~57 | 1.7B / 7.9M |